Even if you prefer spending your time on your core business, accounting is a must. In particular, the income statement (or profit and loss account) is not only a necessary evil, but it also helps you make your company more successful. It shows you whether your company has generated a profit or loss. In this article, you will learn how to create an income statement and how it is arranged in detail.

The multi-step income statement explained

What is an income statement?

In the income statement, the expenses are compared with the income. The difference (balance) from this comparison shows whether your company has turned a profit or a loss. Therefore, the income statement shows how successful your company has been over a specific period (usually a financial year).

Why do you need to create an income statement?

In Switzerland, according to the Swiss Code of Obligations Art. 958 OR, the law stipulates that every company with an annual turnover of over CHF 100,000 in its annual financial statements must present a multi-step income statement for the corresponding financial year. It is fundamental to the correct calculation and payment of taxes and helps meet compliance requirements. Together with the balance sheet and the notes, it ensures "that third parties can make a reliable assessment" (Art. 958 (1) OR).

In addition, your company benefits from accurately kept income statements in a variety of ways. Above all, they provide a detailed overview of all income and expenses over the course of an entire financial year. This helps you assess your financial performance: where have expenses increased compared to the previous year, in which periods was the income particularly high and where is there potential for optimisation in order to remain competitive in the future?

The income statement therefore serves as an important tool for controlling and management. It provides the decisive criteria for ongoing planning and budgeting in your company, for example with regard to production or personnel costs and the margin achieved. In summary: Based on the income statement, you can make informed decisions about investments, cost reductions or growth strategies.

Last but not least, a transparent and accurate income statement promotes the confidence of investors, lenders and business partners in your company's stability and reliability. For bank loan applications, for example, a proper income statement is mandatory.

Single-step or multi-step income statement?

A distinction is made between the single-step income statement and multi-step income statements :

The single-step income statement only conveys income, expenses and the company profit. This allows you to see the financial development of a company quickly and easily.

Here is an example of a single-step income statement:

The multi-step income statement, on the other hand, follows a multi-step process for calculating company profit, in which operating income is separated from non-operating income and expenses. The multi-step income statement therefore shows, among other things, how efficiently a company makes a profit from its main business activity. Therefore, the multi-step income statement offers a particularly good insight into the company's financial situation.

In the following, we will explain the multi-step income statement, especially the two- and three-step income statements, in detail.

The multi-step income statement explained

The multi-step income statement is worked out on the basis of the accounting framework and shows how solid a business is: the interim results of the multi-step income statement, such as gross or operating profit, provide information about profitability and financing of the business.

The multi-step income statements include, among other things, the two- and three-step income statements, which can be shown in report or account form.

About the form of the multi-step income statement

For an annual financial statement to be approved by the auditors, the multi-step income statementhas to meet clear guidelines.

Do you not use proven accounting software and do you create your income statement manually? Then pay attention to a suitable form, so that there are no misunderstandings regarding the interpretation of results and profits:

So that all calculations are discernible, the relevant key figures must be determined properly. For this, the intermediate positions must be clearly marked, for example with a double line or a colour that highlights the individual items and makes them easily visible.

Especially with external audits, for example, an annual balance sheet audit, a high level of order is of great importance so that there are no tax office inspections.

The two-step income statement

A two-step income statement consists of an operating area and a neutral area. The areas summarise the expenses and income and display the company profit at the end. On the left, only the expenses are taken into account, and on the right, the income.

Example of a two-step income statement:

Step 1: The operating area includes, among other things, sales revenues, the use of raw materials and the company's interest expenses. This also includes items, depreciation and amortisation, wages and salaries. The first part of the two-step income statement is completed with the presentation of the operating profit.

Step 2: This is now followed by the neutral area. First, the property income and the property expenses are added/subtracted from the operating profit. As the last item, the direct taxes are deducted. The neutral area ends with the company profit.

The three-step income statement

This determination of profit is made up of three steps in total: like the two-step calculation, the three-step income statement consists of an operating area, a neutral area and, in addition, a trade area.

Example of a three-step income statement:

Step 1: The trade area includes the income and expenses of goods, from which the gross profit is calculated.

Step 2: This is followed by the operating area, in which personnel expenses and depreciation, among other things, are now deducted from the result. At the end of the second area is the operating profit or loss.

Step 3: This is followed by the neutral area, which, in turn, takes into account real estate expenses and income as well as securities expenses and income. After all items are added and subtracted at the end, you obtain the final company profit or loss.

Difference between balance sheet and income statement

With the help of double-entry accounting, you can create both a balance sheet and an income statement. They are the main parts of a company's annual financial statements. But what is the difference? Balance sheet and income statement simply explained:

Balance sheet

On the balance sheet, you can see where your money is coming from and where you have invested it. For this, the assets and liabilities are compared. The balance sheet is based on the reporting date: it shows you your company's assets on a certain date. This makes it particularly suitable, for example, for obtaining information about your current financial situation.

Income statement

The income statement, I/S for short, is different: thanks to it, you can see whether you have achieved profits or losses during a particular period by comparing your income with your expenses. If the right-hand side (income) is higher than the left-hand side (expenses), then you have made a profit in the period under consideration; if it is the other way round, then you have made a loss. For this reason, the income statement is often also referred to as the profit and loss statement.

The following graph illustrates the difference between income statement and balance sheet:

How to create an income statement

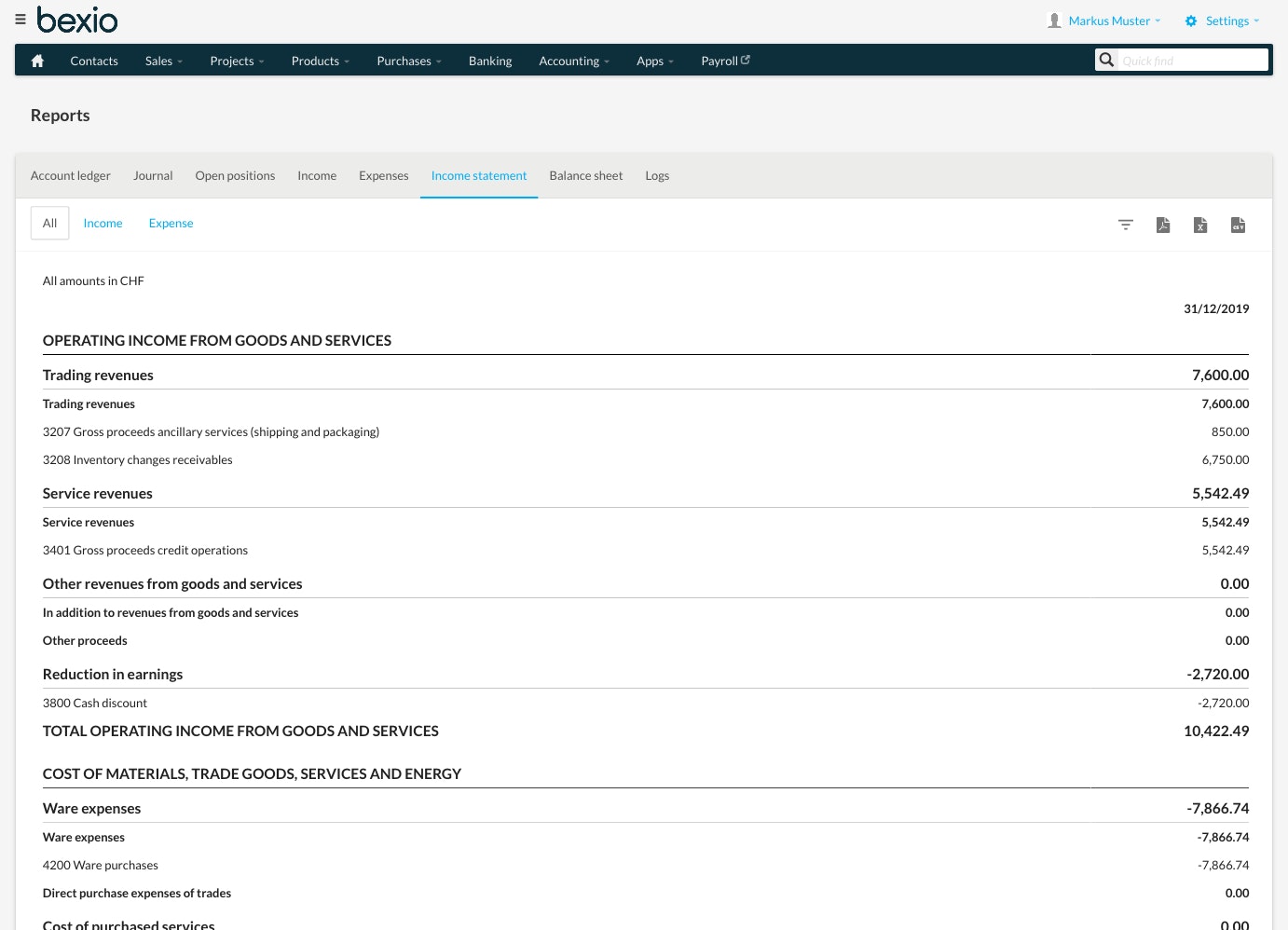

If you use an accounting program, the income statement is usually created automatically for you. bexio, for example, even creates a five-step income statement, which provides far more information than, for example, a two-step income statement. It can be used to see important key figures, e.g. gross profit, EBITDA (earnings before interest, taxes, depreciation and amortisation) and EBIT (earnings before interest and taxes).

Download a sample of an income statement created with bexio as a PDF.

With bexio, you can also have an income statement shown at any reporting date with just one mouse click and download it directly as a PDF. Both the balance sheet and the income statement are financial statements, which are usually only created at the end of a financial year. In practice, however, interim financial statements during the year are also useful: this allows you to quickly assess whether your company is operating within the fixed budget.

Frequently asked questions about the income statement

What is the vertical representation form of the income statement?

The vertical representation form shows the income statement as a clear and simple, continuous list. It is preferably used for internal reporting and for SMEs and shows how the individual income and expense items affect the overall result. All items are listed one after the other – first the sales revenues, then the expense types. The overview is divided into subtotals for gross profit, operating profit and profit before taxes, before providing a net result.

What is the report form of the income statement?

The report form, also called the account form, shows income and expenses in two separate columns – one for income and one for expenses. The direct comparison makes the source and use of the funds clearly visible. This detailed breakdown of the different types of income and expenses is often used for external reporting and for larger companies, as it allows for a deeper analysis of the financial data.

Vertical representation or report form: How should I create the income statement?

Individual companies and partnerships may choose between both forms. Larger companies or corporations must use the report form. The vertical representation form is simpler and more straightforward. The report form offers a clear separation of the different types of income and expenses as well as more details for in-depth analyses. The vertical representation form is suitable for internal purposes and enables you to understand the figures presented quickly, while the report form is more advantageous for external stakeholders such as investors and lenders.

What is the seven-level income statement?

The seven-level income statement is a detailed, structured form of the income statement, shown in the vertical representation form. It divides the income statement into seven main levels to provide a detailed understanding of a company's financial performance. The seven levels are:

- Sales revenues: All income from the sale of goods and services before deductions.

- Use of goods or materials: Direct costs of the goods sold or the materials required to provide services.

- Personnel expenses: All costs associated with the employment of personnel.

- Other operating expenses: All other expenses incurred for the business (rent, insurance, administrative costs, etc.).

- Operating result (EBIT): Profit or loss from the business operation before taking into account interest and taxes.

- Financial result: Income and expenses from financial activities such as interest, dividends and similar items.

- Profit before taxes: Profit or loss before taxes – summarises the business operation and the financial result.

Test the No. 1 in Switzerland now

30 days free and without obligation.